How to Calculate Rental Yield in NZ (And What's Actually a Good Return)

Rental yield is the one number that tells you whether your investment property is actually working. Most people either don't know how to calculate it or they're using the wrong version of it.

Here's a plain-English breakdown.

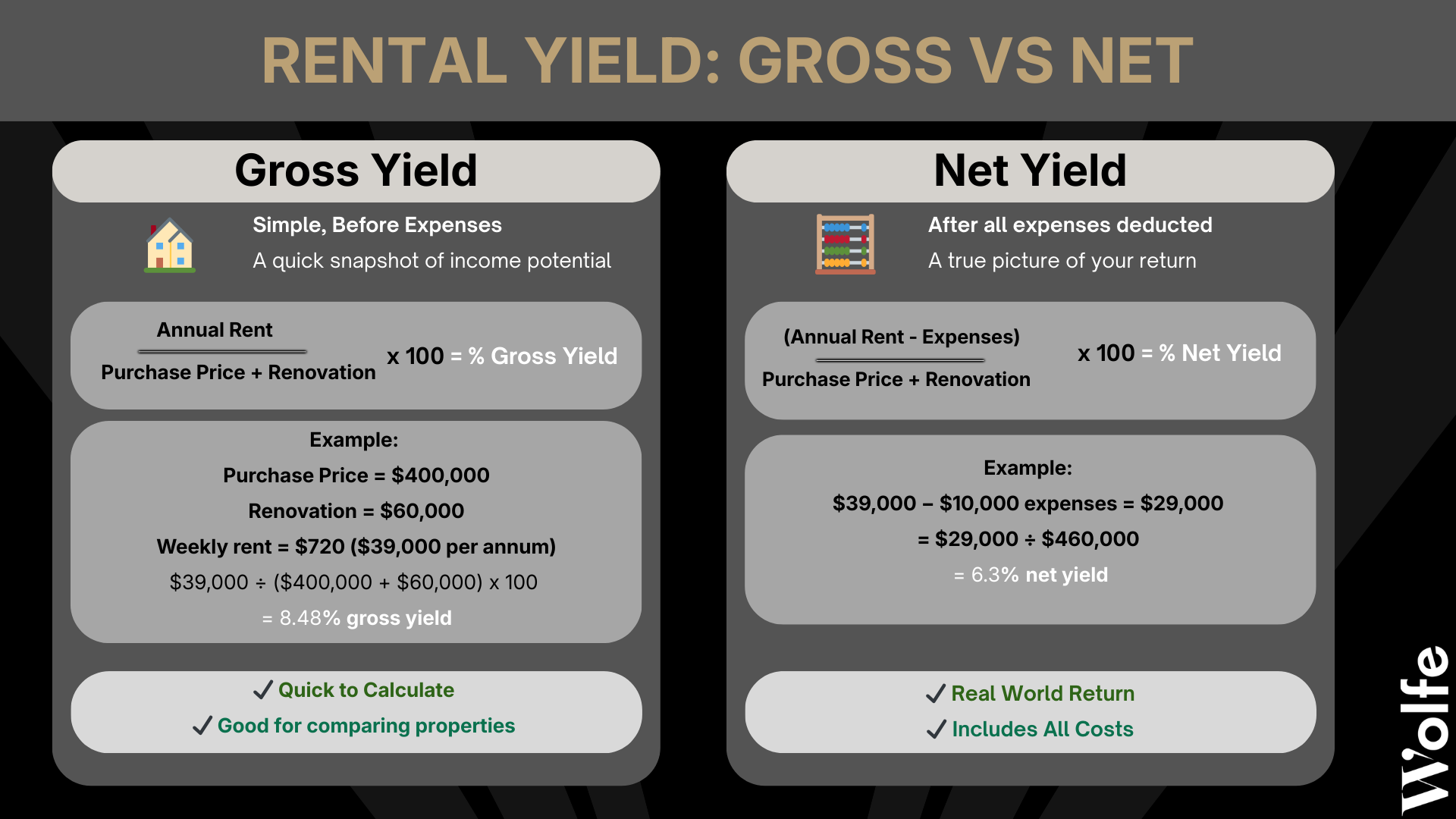

Gross Yield vs Net Yield - What's the Difference?

Gross yield is annual rent divided by the total investment (property purchase price + any renovation spend).

Net yield takes the annual rent, subtracts annual expenses first, then divides by the total investment.

Annual expenses typically include property management fees, insurances, rates, and maintenance.

A rule of thumb is net yield is about 2% lower than gross yield.

What's a Good Rental Yield in NZ Right Now?

The national average gross yield sits at around 4.1 – 4.5%.

Simple benchmarks:

Under 4% → very cashflow negative at current rates

4–6% → likely cashflow negative at current rates

6-8%+ → break-even territory

8–10%+ → genuinely cashflow positive

10%+ → high-performance (achievable with the right strategy)

The Uncomfortable Truth

At current mortgage rates, most NZ rental properties are cashflow negative; even at 7% gross yield.

That's why yield isn't just a metric. It's the difference between a property that funds your future and one that quietly drains your salary every month.

The investors winning right now aren't the ones who got lucky with timing. They're the ones who engineered their yield through smarter buying and targeted renovation.

Real Case Study: 10.5% Gross Yield From a Property Nobody Else Wanted

This deal shows exactly what's possible when you combine the right opportunity with the right plan.

The property: six units in New Plymouth, bought off-market for $1.35 million.

It came with inherited illegal works - the kind of compliance issues that would have scared most buyers away, and almost certainly kept it off Trade Me entirely.

But that's exactly what made it an opportunity.

The Plan

Rather than walking away from the complexity, the Wolfe Property team worked with the clients to:

Correct all compliance issues

Add bedrooms where the market demanded them

Maximise the rental return across all six units

The Result

Before

Annual Rent $87,000

Purchase Price $1,350,000

So an original gross yield of 6.4%

After

Annual Rent $174,000

Purchase Price + Renovation = $1,665,000

Gross Yield - 10.5%

Annual rent doubled. The property was revalued at $2.165 million - creating over $500,000+ dollars in net equity gain, in just a few months.

Why Off-Market Deals Change the Equation

This deal never would have worked at retail price with a bidding war on Trade Me

The illegal works scared off most buyers. But for a team who knew how to price the risk and execute the fix, it was a high-conviction opportunity hiding in plain sight.

That's the Wolfe Property approach: find properties the market misprices, apply a clear renovation strategy, and manufacture the yield - rather than hoping the market delivers it.

4 Questions to Ask Before You Buy

What's the gross yield? (Annual rent ÷ total investment including reno)

What's the net yield? (After all expenses)

Does it still work if rates rise 2%? (Stress-test it)

What could rents be post-renovation? (This is where the opportunity lives)

What Should You Be Targeting?

At Wolfe Property, the benchmarks are:

Accelerate (single dwellings): 8%+ gross yield

Boardroom (multi-units): 10%+ gross yield

Not pie-in-the-sky numbers. They're what happens when you buy the right property with a clear plan, as the New Plymouth case study shows.

Wolfe Property Clients outside New Plymouth Property at Reno Road Tour

Want to see more deals like this? View all case studies →