Across the Ditch

How Australians and Kiwi expats are building cashflow property portfolios in New Zealand - while Australia taxes investors out.

Two countries, moving in opposite directions

The smart-money question for a property investor isn't "which suburb?" - it's "which country?"

Here's why New Zealand keeps coming up: no stamp duty, no land tax, and cheaper money - and Australians can buy freely. New Zealand has no capital gains tax of its own either, and our hold-and-refinance strategy means you don't trigger a capital gains event along the way. Across the Tasman, Australia is heading the other way: negative gearing wound back, the CGT discount ending, surcharges climbing, rates rising.

Australia Australia |  New Zealand New Zealand | |

|---|---|---|

| Stamp duty One-off state tax paid upfront when you buy - often tens of thousands | Payable (varies by state) | None |

| Land tax Annual state tax on the land you hold, every year you own | Payable + rising foreign-owner surcharges | None |

| Capital gains tax | More tax coming - 50% discount ends 1 July 2027, replaced by indexation + a minimum tax | None if held 2+ years (sold sooner, it's taxed); AU residents still taxed by the ATO* |

| Official interest rate RBA cash rate vs RBNZ Official Cash Rate (OCR) | 4.35% - three hikes in 2026 already | 2.25% - on hold |

| 1-year fixed mortgage rate | Around 6%+ | From 4.65% |

| Can you even buy? | Foreigners banned from established homes to ~2029 | Australians can buy freely |

*General information comparing the two countries' tax systems, not personalised financial advice. If you remain an Australian tax resident, Australia still taxes your worldwide income and gains - check with your accountant for advice on your situation. Rates as at July 2026: RBA / RBNZ; advertised 1-year fixed rates, major banks.

As an Australian citizen, you are exempt from New Zealand's foreign-buyer ban. You can buy residential investment property in NZ freely - no special visa, no approval process. Most other overseas buyers can't. That door was never closed to you.

But aren't the yields lower in New Zealand?

Fair question - and the honest answer is the whole point.

Off the shelf, often yes. New Zealand's average rental yields are lower than Australia's regional cashflow hotspots. If all you wanted was a high-yield property to buy and hold, you could find one in regional Queensland.

That's not the opportunity here. We don't buy retail yield - we generate it. Our deals target 8%+ gross yield on single homes and 10%+ on multi-unit projects through renovation and the BRRRR strategy - buy, renovate, refinance and hold, where the return comes from the deal itself, not a tax break.

The market hands you ~3-4%. We manufacture 8-10%+ through renovation.

Cashflow Hacking™: we add the value in

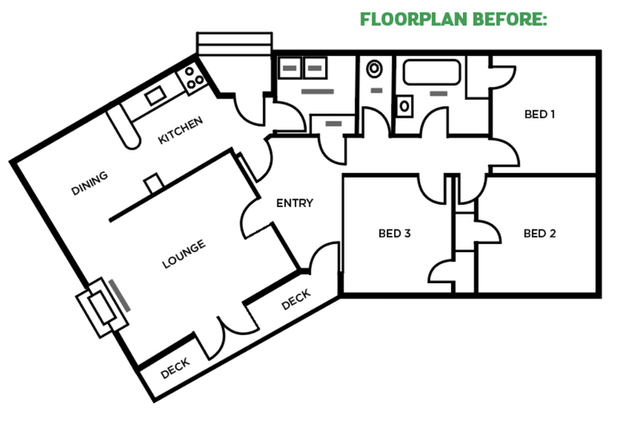

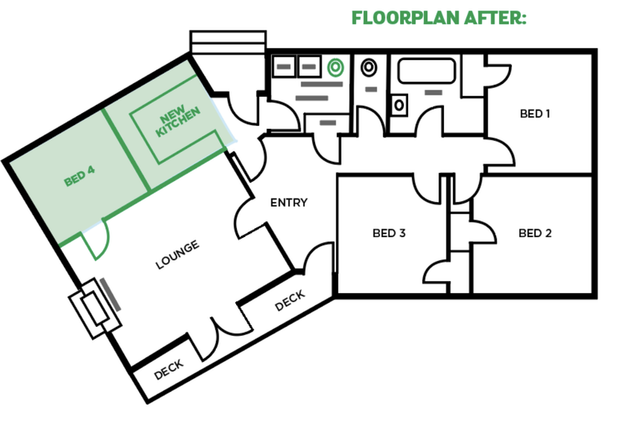

Our whole approach rests on one move: buy an ordinary existing house, then renovate to add value - most often by adding a bedroom within the existing footprint.

A standard 3-bedroom rental earns 3-bedroom rent. But plenty of homes are hiding a 4th bedroom in an oversized lounge or an underused garage. Add it, and the same house re-rents and re-values as a 4-bedroom - lifting both the rent and the property's worth, without extending the building.

Bedrooms move both rent and valuation more than almost any other change you can make. Adding one inside the existing walls is low-cost and fast - and it's what turns an average rental into a high-yield one. It's the single highest-return improvement in most NZ deals.

The BRRRR engine: each deal helps build the next

Adding value is step one. The BRRRR strategy - Buy, Renovate, Rent, Refinance, Repeat - is how one good deal grows into a portfolio over time.

- Buy Off-market where we can. Over half of our clients buy properties the public never sees, through relationships built over years.

- Renovate A targeted, costed value-add - usually that extra bedroom - that lifts the rent and forces equity, delivered by vetted local builders and trades.

- Rent Re-let at the new, higher market rent the renovation unlocked - income that pays you and strengthens your servicing.

- Refinance Revalue the property and release some of the equity the renovation created - funds you can put toward your next deposit.

- Repeat Roll that released equity and the stronger rental income into the next purchase. Each deal makes the next one easier.

Thinking about a new build? Do your research first

Right now, plenty of developers and buyers' agencies are pushing New Zealand new builds to Australian investors. Here's what they won't tell you:

Source: RNZ, May 2026 (CoreLogic data). Apartments are worse: 41% resell at a loss.

| A new build | Our way (value-add) | |

|---|---|---|

| What you pay | Full retail + the developer's margin | Existing property, often off-market |

| Equity at purchase | None - you paid market | Instant, manufactured by the reno |

| Gross yield | ~4%, usually cashflow-negative | 8-10%+, cashflow-positive |

| The market | Oversupplied and discounting | The reno makes the return, in any market |

| Leans on | Tax perks and hoped-for capital growth | The renovation, not a tax break |

A new build makes you the developer's exit. We make you the investor - buying existing property and manufacturing the return yourself. You own the margin, not the developer.

Kaveen: a tired 3-unit block turned into a 10%+ cashflow machine

A multi-unit, done-for-you project we sourced, renovated and tenanted end to end for an Australian investor - while he stayed in Australia the whole time.

89 Glenpark Ave - three units, fully renovated by our Power Team.

| Purchase price (3 units) | $700,000 |

| Renovation spend | $150,000 |

| Revaluation | $1,300,000 |

| Equity created | ~$450,000 |

| New rent | $560 / unit / week |

| Gross yield | 10%+ |

"While residing in Australia, I needed someone I could trust to handle the entire process - from sourcing the right property to managing a full-scale renovation - and she exceeded my expectations in every way."

Christchurch: $175,000 of equity from one renovation

This client invested remotely - leaning on our coaching and Power Teams rather than being on the ground - and turned a tired, low-yielding rental into a high-performing one.

We bought a standard Christchurch home and scoped a targeted value-add renovation, then re-let it at the new market rent. The property revalued well above its all-in cost, the rent climbed 83%, and the gross yield landed above 8%.

| Purchase price | $420,000 |

| Post-renovation valuation | $650,000 |

| Net equity gain | $175,000 |

| Annual rent | $20,800 → $38,000 (+83%) |

| Gross yield | 8%+ |

You don't have to live where you invest

80% of our clients already invest in New Zealand regions they don't live in. Whether you're in Brisbane, Perth or Balclutha makes no practical difference - the whole model is built to run remotely.

From Whangārei to Dunedin, every project runs through vetted local Power Teams - brokers, builders, trades, property managers and agents. They are your eyes, hands and feet on the ground, so you can buy where the best deals are, not just where you happen to live.

Hands Free: we build your New Zealand portfolio - you just own it

Our Hands Free service was built for time-poor CEOs, All Blacks and other professional athletes who wanted everything property builds - without the time, or the learning curve. Today it's open to any qualifying client, and it's tailor-made for investing from Australia.

Hands Free means our team drives the entire deal on your behalf - sourcing (often off-market, before the public ever sees it), negotiating, planning and project-managing the full renovation. You stay in control of the outcome without ever being on the tools or on site.

Accelerate Hands Free

Your first NZ deal done for you. A single home, value-add, targeting 8%+ gross yield. The on-ramp.

Boardroom Hands Free

Our flagship. Multi-unit, portfolio-level projects targeting 10%+ gross yield, fully managed, for investors ready to move serious capital.

From $5,000 to a $20M portfolio - built from scars, backed by results

Ilse Wolfe went from $5,000 to a multi-million-dollar portfolio before 40 - but the lesson that built this business came from a mistake.

For her first five years she was on the tools, buying and holding 10+ properties while chasing capital growth and ignoring cashflow. It caught up with her: the family ended up in a cashflow hole deep enough that they moved in with the in-laws to dig out. As she puts it, you can't buy groceries with capital gains. That's when she built the Cashflow Hacking™ framework - and rebuilt, into 30+ rentals that pay her. Featured in the NZ Herald, BusinessDesk and on 1News.

"Focus on cashflow and the equity follows. The portfolio should fund your lifestyle - not the other way around."

The window is widest right now. Let's talk about your first deal.

Book a free, no-obligation 15-minute call. We'll look at your goals and position, and show you what a New Zealand cashflow portfolio could realistically look like for you.

See if we're a fit →Prefer to read later? Download the PDF guide

Wolfe Property Coaching provides property investment coaching and education. It is not financial, tax, or legal advice and does not constitute a recommendation to buy any specific property. Australian and New Zealand tax settings referenced reflect publicly reported policy as at July 2026 and may change - please seek independent professional advice for your circumstances. © 2026 Wolfe Property Coaching.